"Beyond Basics: Advanced Insights into Optimizing Input Tax Credit under GST"

Introduction:

Input Tax Credit (ITC) is a key feature in the Goods and Services Tax (GST) system, offering businesses a powerful tool to enhance financial efficiency. This article explores strategies for businesses to leverage ITC effectively and maximize the associated benefits.

Understanding Input Tax Credit:

Input Tax Credit allows businesses to offset the tax they have paid on inputs against the taxes they are liable to pay on their outputs, thus avoiding a cascading tax effect.

Example:

Say, you are a manufacturer - tax payable on output (FINAL PRODUCT) is Rs 450 and tax paid on input (PURCHASES) is Rs 300, you can claim Input Credit of Rs 300, and you only need to deposit Rs 150 in taxes.

See here:

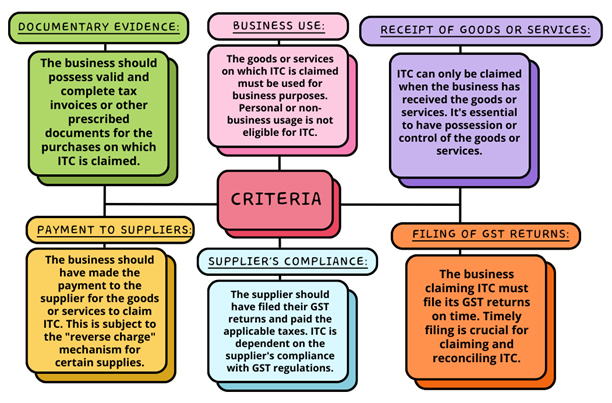

To claim Input Tax Credit (ITC) in the Goods and Services Tax (GST) system, businesses need to meet certain criteria. Here are the key requirements:

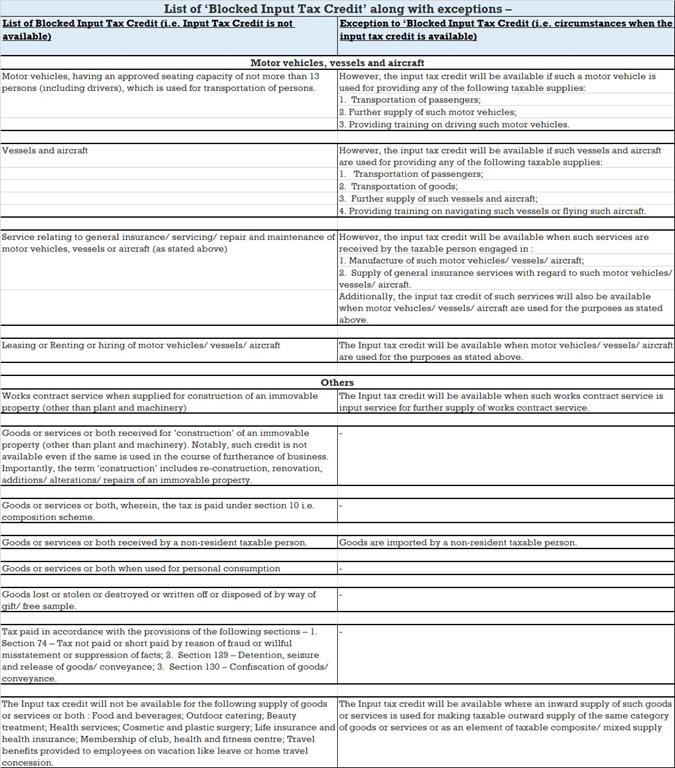

Blocked Credit:

In the landscape of Goods and Services Tax (GST), it's important for businesses to grasp the details of Input Tax Credit (ITC) to smoothly handle tax complexities. One thing we need to focus on is Blocked ITC – a situation where claiming credits becomes a bit complicated.

Overview of Blocked ITC:

While GST has transformed the tax system, specific conditions hinder the seamless flow of Input Tax Credit. For businesses, it's crucial to understand these restrictions in detail to ensure compliance.

Unveiling Specific Cases:

Reversal of ITC:

When Reversal Becomes Necessary:

Reversal of ITC occurs under specific circumstances outlined in GST rules. Understanding these situations is key to avoiding inadvertent non-compliance. Common instances include:

- Non-payment to suppliers: if a business fails to pay its suppliers within the stipulated time, ITC claimed on those invoices many need to be reversed.

- Exempt Supplies: When a business deals with both taxable and exempt supplies, it must proportionately reverse the ITC related to exempt supplies.

- Blocked Credit Scenarios: Certain goods or services are explicitly mentioned as ineligible for ITC. Any credits claimed on such items might need to be reversed.

- Other Cases:

Where any registered person who has availed ITC:

- opts to pay under composition scheme (Sec 10) or

- Where the goods or services or both supplied by him become wholly exempt or

- Has Cancelled the Registration

Then he shall pay an amount, by way of debit in the electronic credit ledger or E-cash ledger, equivalent to the credit of input tax in respect of:

- Inputs held in stock and

- Inputs contained in semi- finished or

- Inputs contained in finished goods held in stock and

- Capital goods, reduced by such percentage points as may be prescribed.

Proviso: After payment of such amount, the balance of ITC, if any, lying in E-credit ledger shall lapse.

Cross-Utilization of ITC:

ITC can be cross utilized between the Integrated GST (IGST), Central GST (CGST), and State GST (SGST) components, but it must be in accordance with the GST laws.

Restriction on use of amount available in Electronic Credit Ledger:

Rule 86B limits the use of input tax credit available in the electronic credit ledger for discharging output tax liability.

Applicability of Rule 86B:

This rule is applicable to the registered person having value of taxable supply (Other than exempt supply and zero-rated supply) in a month exceeding 50 Lakh.

Nature of restrictions imposed:

The registered person to whom the said rule is applicable cannot utilize input tax credit in excess of 99% of the output tax liability.

Exemptions to Rule 86B:

- Payment of Income tax more than Rs. 1 lakh.

- Receipt of refund of input tax credit in case of Zero-rated supply & Inverted Tax Structure of more than Rs. 1 Lakh.

- Specified registered persons:

- Government Department, or

- A public sector undertaking, or

- A local authority, or a statutory body

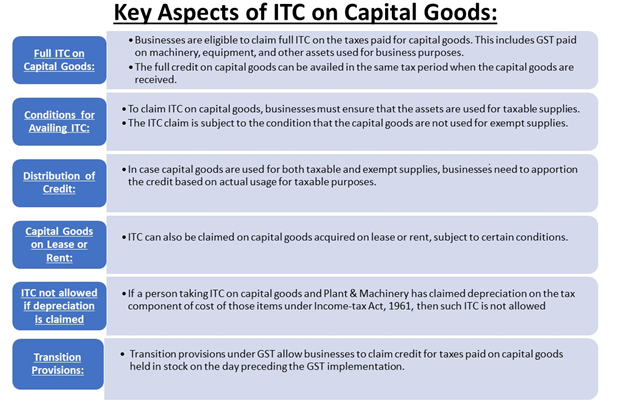

ITC on Capital Goods

One of the key features of GST is the input tax credit (ITC) mechanism, which allows businesses to claim credit for taxes paid on inputs and capital goods. In the context of the capital goods sector, understanding the implications of GST on ITC becomes crucial for businesses.

Transfer of Credit:

Where there is a change in the constitution of a registered person on account of

- Sale

- Merger

- Demerger

- Amalgamation

- Lease or transfer of the business

With the specific provisions for transfer of liabilities, registered person shall be allowed to transfer the ITC which remains unutilized in his electronic credit ledger to such sold, merged, demerged, amalgamated, leased.

Time limit for availing ITC by registered person

Time limit is EARLIER of: -

- 30th November following the end Financial Year to which such invoice or debit note pertains or

- Furnishing of the relevant annual return.

Exception: Time limit does not apply to re-availing of credit that had been reversed earlier

Penalty on Wrong Availment of ITC Under GST

As per the GST provisions, if an entity wrongly avails ITC, it must reverse the credit; failure to comply will result in the imposition of interest and penalties.

Interest Component:

Interest will be charged on ITC wrongly availed and utilized; Thus, interest will apply only when ITC is both claimed and utilized.

Penalty Amount:

If ITC is wrongly availed or utilized, the penalty can range up to 100% of the ITC amount availed or INR 10,000, whichever is higher.

GST Act clarifies that penalty can be levied for ITC wrongly availed or utilized. Thus, even if ITC is availed but not used, a penalty may still be applicable. Thus, implying that penalty is chargeable on ITC wrongly availed but not utilized also.

Conclusion:

In conclusion, businesses need to understand the rules that come with claiming Input Tax Credit under GST. Staying informed, consulting with tax professionals, and adapting to the evolving regulatory landscape will empower businesses to optimize their tax compliance strategies.

Call to Action:

Let's embark on this journey of GST compliance with a proactive approach. Regularly updating ourselves on the latest GST amendments and seeking professional advice will empower businesses to not only navigate the complexities but also to thrive in the ever-changing tax environment.